Image by Gerd Altmann from Pixabay

The Innovation Bank is an autonomous network platform applicable to all branches of technical services enterprise. The platform is governed by game theory, actuarial math, and blockchain technology. The purpose is to capitalizing the STEM professions.

The Innovation Bank Project Overview

The objective is to reward individual practitioners to establish physical facts in collaboration with other practitioners. Knowledge, innovation, and wisdom may be discerned from these interactions. Where such metrics exist, intangible “in-situ” knowledge assets may then be capitalized in a manner analogous to how tangible assets are capitalized in the existing economic system.

Past research has demonstrated individual components of the Innovation Bank within various for-profit enterprise settings. This current effort is unique in its attempt to integrate these components in an autonomous public network.

Several factors need to be taken into consideration:

Engineering is an essential industry – it is essential that the Innovation Bank is complementary rather than disruptive to existing institutions and operations.

All STEM professionals and practitioners are unified and enabled for cross-discipline interaction.

Practitioners are economically compensated within the platform for their contributions to the Innovation Bank. Compensation is proportional to the value of the contribution.

Practitioners own, control and hold title to their identification, and thus, their specific transaction records.

Specific Outcomes:

The initial funding for The Innovation Bank will result in the production of a minimum viable product comprised of an operational native blockchain with decentralized governance, algorithmic token allocation, and database auditing system (block explorer). These outcomes will be suitable for research, analysis, development and future growth within the professional and academic STEM communities. This test bed will allow us to develop means, methods, and metrics for advancing the above considerations.

Intellectual Merit:

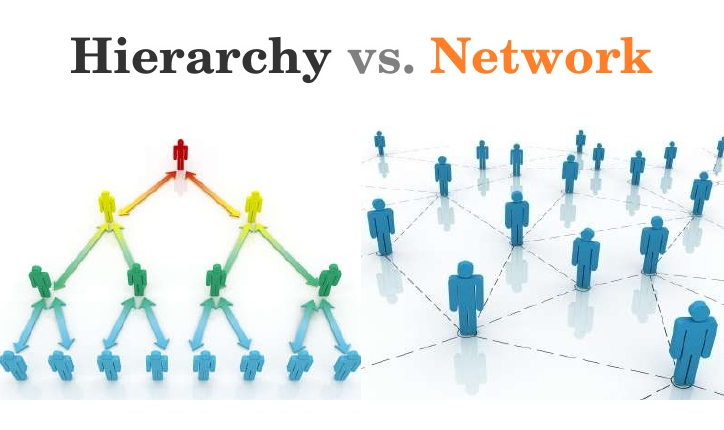

The purpose of the Innovation bank is to unify the STEM professionals in society at large. Typically, STEM professionals are segmented by institutions with mismatched ontologies, competitive restraints, or regulatory limitations. While such hierarchical arrangements were well-serving in earlier times, new tools exist allowing network platforms to efficiently deliver value at speed, and at scale.

The core activity of the Innovation Bank is to develop worthy claims such that a qualified validator would be willing to be permanently and immutably associated with the claimant. This union forms a node with two branches for which each would be compensated in proportion to their total stake in the system. A network graph is thus formed from the interconnectivity of aggregate nodes and branches.

The dominant game strategy for each individual would be to allocate knowledge resources to where they are needed most rather than where profits are most assured. Financial value is derived from the dynamic metadata embedded in the aggregate network yielding business intelligence which would command a premium over static non-validated data.

Broader Impacts:

Economic growth is contingent on technological change – this is the exclusive domain of STEM professionals and practitioners. There is currently no reliable way to directly measure the impact of technological change on economic growth. Pricing and allocation are often irrational. Engineers, scientists, technologists, and mathematicians, serve to remove risk from complex systems ranging from consumer products to public infrastructure and the natural environment.

The Implications of the Innovation Bank includes the reduction of systemic risks and improved allocation of natural and intellectual resources. In essence, The Innovation Bank will gradually replace Consumption Capitalism with “Preservation Capitalism”. The introduction of a new risk-backed asset class would amplify the missions of existing institutions such as universities, corporations, finance, insurance, and government.

Given a game that everyone can potentially win, universal engagement in STEM education and STEM applications would become a dominant social policy strategy. More information can be found at The Ingenesist Project. Please contact us for more information regarding The Innovation Bank Project Overview or please read the the following paper:

The Innovation Bank; Blockchain Technology and the Decentralization of Engineering Professions

The value of engineering is perhaps the greatest arbitrage opportunity in history. After 100 years of regulated professional engineering practice, engineering is still valued on a linear time and materials basis. In the Internet age, where everything and everyone is connected by engineering, I argue that the value of engineering may be accounted by the exponential Network Effect.

The value of engineering is perhaps the greatest arbitrage opportunity in history. After 100 years of regulated professional engineering practice, engineering is still valued on a linear time and materials basis. In the Internet age, where everything and everyone is connected by engineering, I argue that the value of engineering may be accounted by the exponential Network Effect. Anyone who was around in the early 1990’s may remember the mantra of modern globalization was that centralized markets were bad and decentralized markets were good. Fast forward to 2016 and blockchain technology: centralized ledgers are bad decentralized ledgers are good. Does this sound familiar? Blockchain and NAFTA may have a lot in common. The good news is that perhaps this new world is not quite as uncharted as it now appears.

Anyone who was around in the early 1990’s may remember the mantra of modern globalization was that centralized markets were bad and decentralized markets were good. Fast forward to 2016 and blockchain technology: centralized ledgers are bad decentralized ledgers are good. Does this sound familiar? Blockchain and NAFTA may have a lot in common. The good news is that perhaps this new world is not quite as uncharted as it now appears.

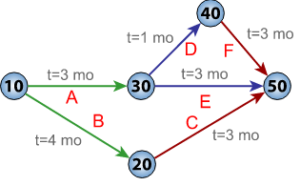

Are blockchains insurable? This question was posed to us as a topic for presentation by the Center of Insurance Policy and Research, a research arm of the National Association of Insurance Commissioners (CIPR / NAIC)

Are blockchains insurable? This question was posed to us as a topic for presentation by the Center of Insurance Policy and Research, a research arm of the National Association of Insurance Commissioners (CIPR / NAIC) On a critical path.

On a critical path.

The hallmark of a great society is the ability to capitalize it’s needs, not it’s arbitrage opportunities. The Highest and Best Use for Blockchain Technology must be to reduce the cost of capital by decentralizing risk, not necessarily money…yet

The hallmark of a great society is the ability to capitalize it’s needs, not it’s arbitrage opportunities. The Highest and Best Use for Blockchain Technology must be to reduce the cost of capital by decentralizing risk, not necessarily money…yet On a sour note, the Bitcoin protocol now provides a way for Insurance Company Executives to eliminate countless brokers and administrators from the balance sheet as computer algorithms are now capable of performing many of the same tasks. On the other hand, these same executives are being asked to provide insurance to clients who intend to do exactly that; replaced countless brokers and administrators with a computer algorithms. Can these companies identify the risk exposure to their selves and their client? Can an actuarial scientist calculate the probability that any number of perils will manifest? If so, does anyone truly understand the consequences of a crypto-block-coin meltdown? I didn’t think so.

On a sour note, the Bitcoin protocol now provides a way for Insurance Company Executives to eliminate countless brokers and administrators from the balance sheet as computer algorithms are now capable of performing many of the same tasks. On the other hand, these same executives are being asked to provide insurance to clients who intend to do exactly that; replaced countless brokers and administrators with a computer algorithms. Can these companies identify the risk exposure to their selves and their client? Can an actuarial scientist calculate the probability that any number of perils will manifest? If so, does anyone truly understand the consequences of a crypto-block-coin meltdown? I didn’t think so. As the Uber/Lyft business model continues to hone its end-run around the heavily regulated taxi industry, many are now looking at the air transportation industry for vulnerability to Uberesque disruption. Enter Uber Airlines.

As the Uber/Lyft business model continues to hone its end-run around the heavily regulated taxi industry, many are now looking at the air transportation industry for vulnerability to Uberesque disruption. Enter Uber Airlines.{kind=link}